Stock Pick of the Week: Bill.com ($BILL)

Is the intelligent SMB payments platform Bill.com worth investing in?

For those joining in for the first time, welcome! Pocket Change is a newsletter where Tony + Karine keep track of and analyze stocks we think are noteworthy (and whether we should invest pocket change into). We’ve been friends since 2013, and have been sending each other stock suggestions and portfolio screenshots over the years. Pocket Change is our way of opening up the conversation and sharing these ideas more publicly. This newsletter goes out every weekend with our analysis and decision for a new stock.

To receive this newsletter weekly, consider subscribing 👇

Summary

☁️ Cloud-based software for SMBs to pay vendors, approve bills, and collect money from customers

📍IPO’d in Dec 2019 at $35

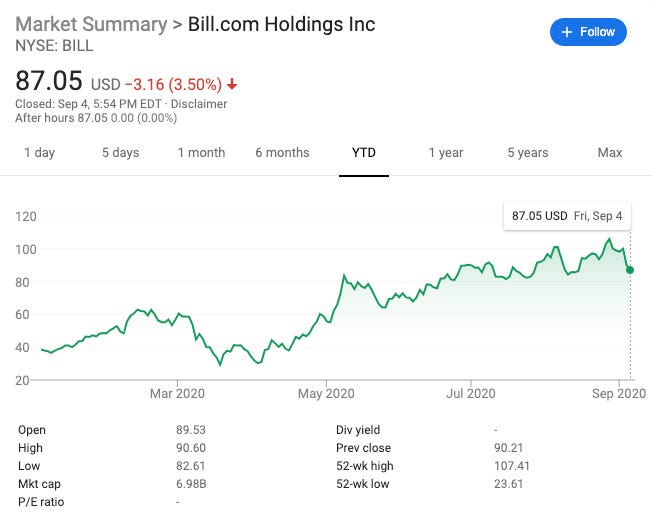

🔥Stock price up +164% YTD

💰Enterprise Value: $6.28B

📈FY20 Revenue: $157M, up 31% YoY

Bill.com has been one of the hottest companies this year, with its share price increasing 164% year-to-date. Last week, the company reported stellar results, with revenue increasing 33% compared to the prior year. However, the expectation was high for a strong “beat” of the estimated 20% provided by Wall Street analysts, and so the stock dropped after the announcement.

Nevertheless, we think these are solid growth numbers at a time when small and midsize businesses (SMBs) are struggling with COVID-induced shutdown and unlikely to invest in new technology, and a pull-back in the share prices could be a way to invest in an attractive business for the long term.

What is Bill.com?

Founded in 2006, Bill.com provides cloud-based software for SMBs to pay vendors, approve bills, and collect money from customers. Additionally, Bill.com services accounting firms (over 70+ of the top 100 accounting firms) by helping them grow their book of business by automating bookkeeping tasks on behalf of customers. Banks also use Bill.com to provide their customers with a digital solution around cash flow management. Today, over 98,000 customers use Bill.com to manage their financial workflows and process their payments, totaling $96.5 billion during fiscal 2020.

Fundamentals

EV: $6.28B

EV/NTM Revenue: 34x

FY20 Revenue: $157M, up 31% YoY

Net Dollar Retention Rate: 121%, 110% and 106% during fiscal 2020, 2019 and 2018, respectively.

Payback Period: 15 months

How Bill.com makes money

The Bill.com product automates complicated workflows for businesses that receive and pay invoices. Legacy solutions could involve paper invoices, Excel-based tracking, and even paper checks being mailed to vendors. By automating this process, Bill.com saves SMBs time, reduces errors, and creates a network of vendors embedded into their platform.

Subscription and Transaction Revenue (92% of Total). Bill.com primarily makes money by offering their product as a subscription service to SMBs. They also partner with companies that already provide financial services to SMBs, such as banks and accounting firms to create white-label solutions. For example, last year they worked with KeyBanc to launch a solution called Key CashFlow. Overall, Bill.com makes ~$1,500 in annual revenue per customer (ARPU).

Interest on Funds Held for Customers (8% of Total). Bill.com also temporarily holds a lot of cash for their customers. In the last quarter, total customer funds increased by 23% to $1.6 billion.They are able to invest the funds in liquid investment securities, but this tends to be a volatile revenue stream and the company excludes this when reporting their headline growth numbers.

Growth opportunities

The business has few natural growth levers as SMBs grow larger, their transaction volume increases with their vendors. On the flip-side, as more vendors join their platform, it deepens the stickiness of Bill.com for their entire ecosystem. This expansion is reflected in their dollar-based net retention rate, which was at 110% but accelerated to 121% in the last quarter. Additionally, it

The current total addressable market for Bill.com is $39 billion, assuming the same ARPU multiplied by the 6 million and 20 million U.S. and global small medium business. However, given the innovativeness of Bill.com and their platform, we wouldn't be surprised if they can significantly increase their ARPU to beyond ~$1,500 into their adjacent markets such as accountable receivable/payable financing.

Competitors / Risks

Competition: Bill.com has various competitors that go after SMBs, from larger enterprises like SAP, Sage Intacct, and Netsuite but also startups like Expensify that focus mostly on receipt and expense management (and not necessarily invoices). Accounting software tools like Freshbooks, Xero, and Quickbooks also provide some sort of AP and AR management but don't seem to act as direct competitors. Newer startups like Stripe, Tipalti, and more are also competitors that have begun building out parts of Bill.com’s product.

Slowing Growth + Unprofitable: Bill.com is currently unprofitable, with a net loss of $31.1 million in FY2020 and $7.3 million for FY 2019 and a slowing revenue growth rate of from 46% in Q12020 to 32.9% in Q2 2020. Slowed revenue growth is normal for maturing companies, but is a risk to note.

Key Questions to Ask Yourself (before we think you should buy...)

Will Bill.com be able to continue differentiating itself from its competitors and retain its customers?

Top public SaaS companies are trading at 26-32x EV/NTM Revenue and Bill.com’s 34x multiple is quite high. Do you think Bill.com is currently overvalued?

Our Take

While Bill.com is in a growing market and has great a growth trajectory, we think the valuation is a stretch and would recommend investing when the stock has pulled back.

Note this is not investment advice. Please consider doing your own research before making any investments!

If you’re finding this newsletter valuable, consider sharing it with friends, or subscribing and following us on Twitter if you aren’t already. If you have any feedback / comments / suggestions for what you’d like us to analyze, please share with us as well!