Stock Pick of the Week: DraftKings ($DKNG)

Stock Pick of the Week: DraftKings ($DKNG)

How does this fantasy sports betting platform fare during COVID?

For those joining in for the first time, welcome! Pocket Change is a newsletter where Tony + Karine keep track of and analyze stocks we think are noteworthy (and whether we should invest pocket change into). We’ve been friends since 2013, and have been sending each other stock suggestions and portfolio screenshots over the years. Pocket Change is our way of opening up the conversation and sharing these ideas more publicly. This newsletter goes out every weekend with our analysis and decision for a new stock.

This week, we’ve collaborated with Tanay Jaipuria, formerly at a16z and McKinsey, for his expertise and thoughts on DraftKings!

To receive this newsletter weekly, consider subscribing 👇

Summary

🏀⚾🏒♣️🏈 DraftKings: Online Platform to play Fantasy Sports

📈2019 Revenue: $430M

🔥EV/2019 Revenue Multiple: 25.6X

👀 TAM: ~$40B between Online Sports Betting + iGaming

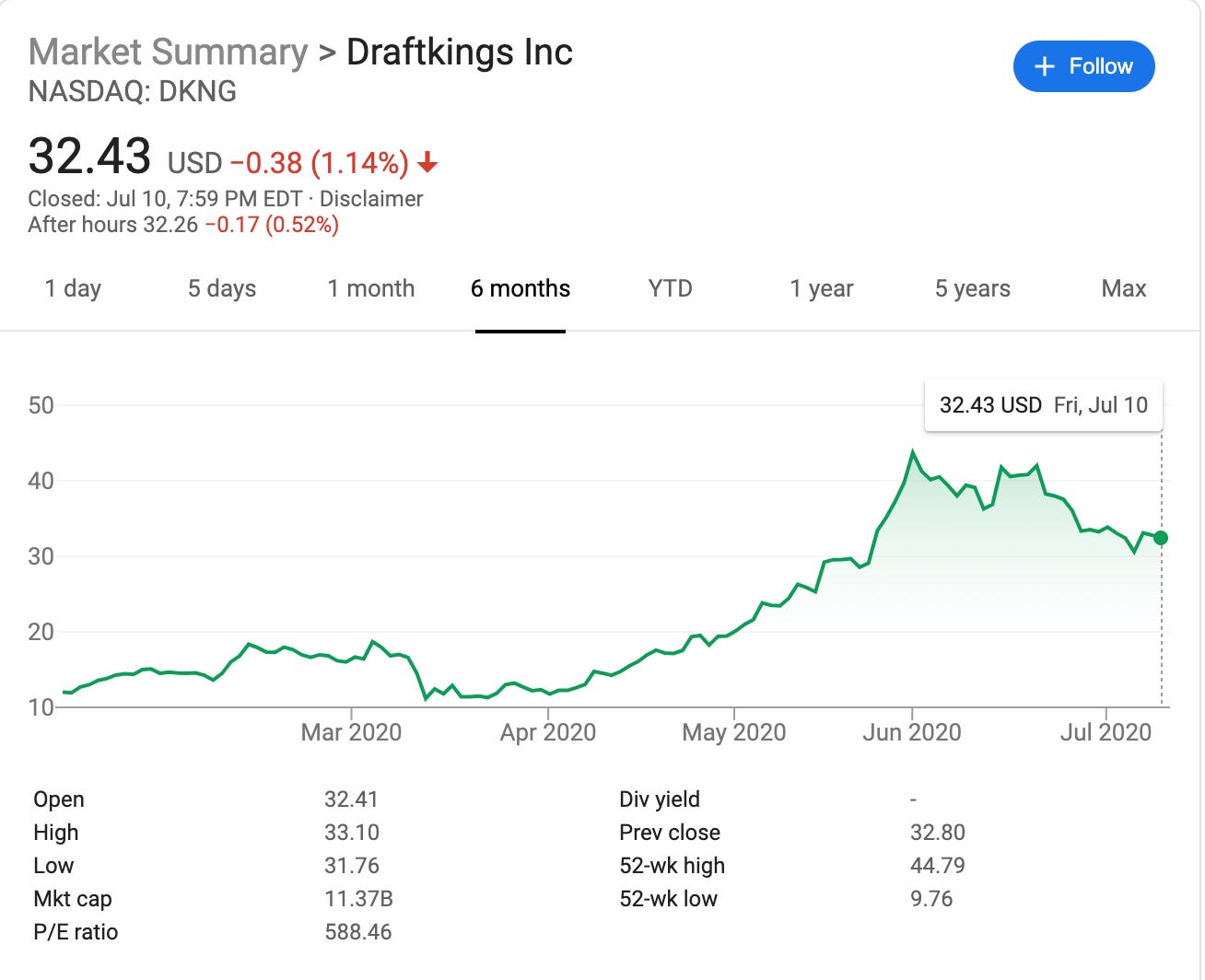

Earlier this year, COVID-19 took a major hit on all sports. For those that have been eagerly awaiting for its return, we’re excited for the possible return of the NBA season in three weeks on July 30 (no guarantees though). However, despite the obvious impact of the coronavirus, DraftKings, a platform to play daily/weekly fantasy sports for cash prizes in a wide variety of sports, like the NBA, NFL, NHL, is near all-time highs on the stock market and up over 80% in a few months since it officially went public at ~$17.50/share.

One thing you may not know is that DraftKings has other fast-growing segments of its business in eSports, iGaming (online casino games such as Blackjack, video poker, etc), and a growing B2B tech side of its business called SB Tech (which we’ll expand on). We’ll take a deeper look at their current fundamentals, growth opportunity and risks to see it’s worth investing in DraftKings.

Did you know?

In 2016, DraftKings reached an agreement to merge with FanDuel, its closest competitor in daily fantasy sports. The Federal Trade Commission reviewed the proposed deal and filed to block it over competitive concerns. The combined entity would own a 90% share of the daily fantasy sports market, a monopoly position.

While choosing to fight the FTC in a legal battle was on the table, DraftKings and FanDuel eventually made the decision to terminate the merger in July 2017.

DraftKings eventually ended up going public earlier this year, not through a traditional IPO but rather through a reverse merger with a Special Purpose Acquisition Company called Diamond Eagle which was already public (and in the process also acquired SB Tech, a gaming and technology company).

Fundamentals

DraftKings today consists of two segments: SB Tech, which it acquired as part of going public, and DraftKings.

The combined entity made $430M in revenue in 2019, with DraftKings making $323M in revenue and SB Tech making $107M in revenue.

DraftKings’ performance in 2020 is very tied to the continued impact of COVID-19 on Sports. While DraftKings has expanded into Esports and other verticals while most sports were shut down, it has still seen a big hit as major sports paused as one might expect. Prior to COVID-19, the DraftKings segment was pacing at 60% a year growth, with SB Tech pacing at 30% per year growth. Instead, DraftKings ended Q1 delivering 30% growth with SB Tech delivering 3% growth. Since the impact of COVID was only felt in the last month and Q2 will take a bigger hit, it’s not unreasonable to think that DraftKings will end the year with single-digit revenue growth, but it should reaccelerate once sports resume and in 2021.

Enterprise Value: $11.05B

2019 Revenue: $430M

EV/2019 Revenue: 25.6X

2020 Revenue estimate: ~$450M

EV/2020 Revenue: 24.6X

One might consider those pretty high multiples, close to most SaaS businesses which have high gross margins and strong revenue retention.

DraftKings had gross margins of ~62% in 2019 but it expects them to decrease over time to ~50% as its business expands in online betting and iGaming, which have revenue shares with casinos (for licenses) and may have higher taxes associated with it.

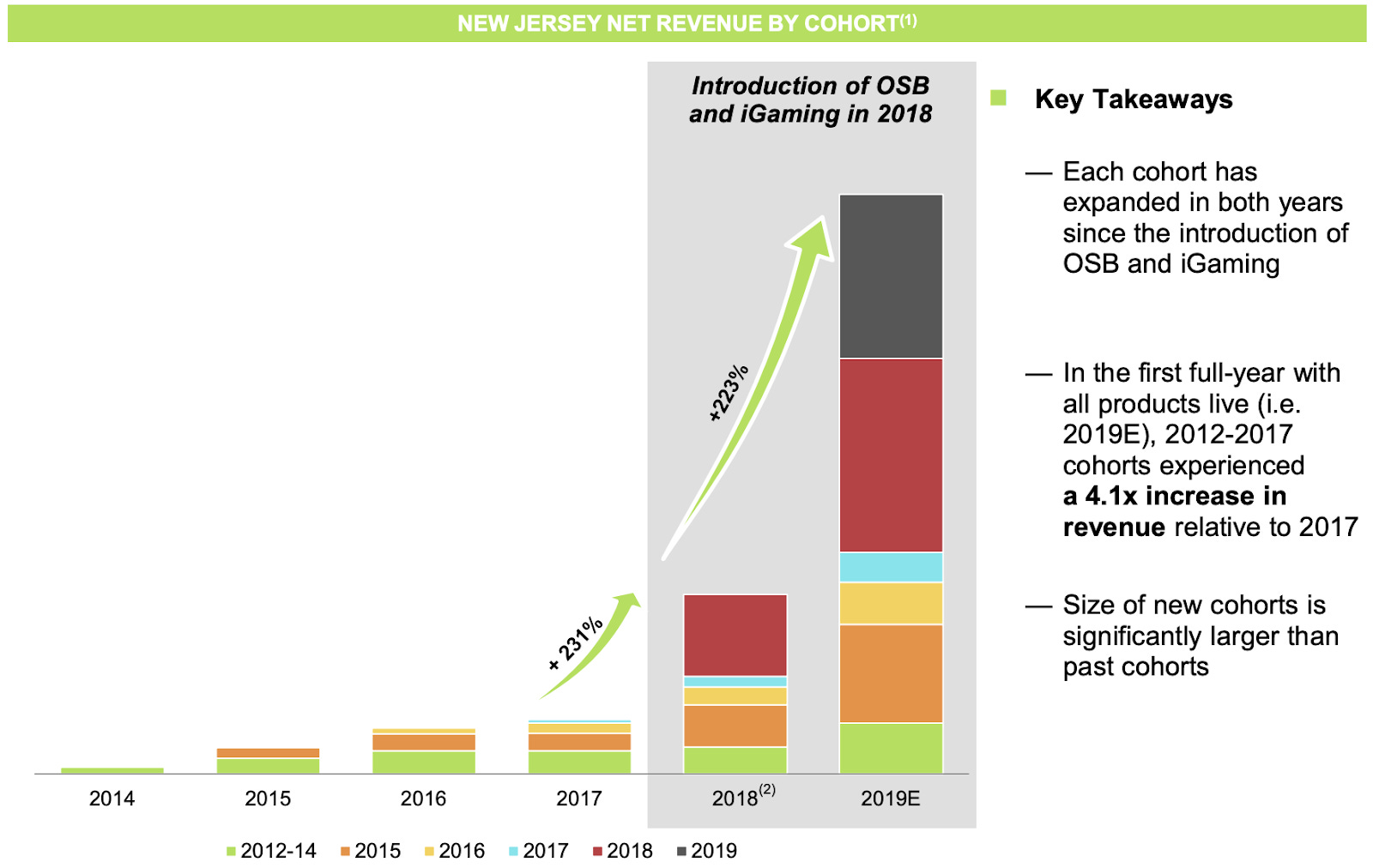

However, promisingly for DraftKings, its customer engagement looks strong. Based on their New Jersey data (where they have their full suite of products launched), customer cohorts are increasing their usage significantly, and new cohorts are heavier users than previous cohorts were. As it expands into these product segments in other states, this could fuel growth in the coming years.

DraftKings expects 30-35% EBITDA margins long-term.

One rough estimate of the growth embedded in today’s stock price is that if you value DraftKings at 30X earnings in 2025, it needs to have ~$370M in earnings in 2025 to justify an $11B enterprise value then (obviously, if you invest you would want the enterprise value to have grown between now and then). Assuming no taxes at the time because of net operating losses and a 30% margin, that means DraftKings needs to do ~$1.25B in revenue in 2025, which is ~23% CAGR over the next five years. Not unreasonable, but DraftKings has also not made a profit yet and so may not be quite there in terms of margin in five years.

New Sponsored Section(!): We wanted to share a new stock investing app we’ve been loving called Public. Public makes the stock market social (think Robinhood meets Twitter - where you can follow other investors, see what they’re investing in, and then actually invest). We’re just starting to add more analyses + our Pocket Change portfolio there, so join us! We may receive compensation from affiliate links.

How DraftKings Makes Money

The DraftKings entity can be seen as having four primary business lines.

1. Daily fantasy sports (DFS) which accounted for ~50% of 2019 revenue. DFS allows users to compete against other users across a variety of sports, typically creating lineups based on the games happening on a given day. DraftKings operates this daily fantasy sports platform and charges a fee of ~10%, handling administration, scoring, matching, and payout. This segment made $213M in 2019, accounting for just half of the total revenue.

2. Online Sports Betting which we estimate accounted for ~18% of 2019 revenue. Online Sports Betting currently on DraftKings is live in seven states, representing 12% of the US population. Currently, online sports betting has been legalized in 14 states (24% of the population) since the repeal of the PASPA act in May 2018. DraftKings has a #1 or #2 position in some of the key states they are in such as New Jersey and Indiana.

3. iGaming (online casino games such as Blackjack, video poker, etc) which we estimate accounts for 7% of 2019 revenue, which is expected to be a ~$20B opportunity in the US, and is also in the process of being legalized across more states over time. Today, DraftKings is live in New Jersey and is #2 by share, despite launching there only a year ago, and taking on incumbents who have been there for five years.

4. SB Tech which accounts for ~25% of revenue, which DraftKings acquired as it went public. SB Tech is a B2B provider of online betting and gaming solutions, and made ~$110M in 2019, with a diverse set of customers across Asia, Europe and North America.

Interestingly, while daily fantasy sports is the core business, long-term we expect it to be more of a channel to acquire customers and then cross-sell them into the more revenue-generating segments of online sports betting and iGaming. Today, about 30% of DraftKings’ online sports betting customers were cross-sold from their DFS service, and 50% of that set of users also used their iGaming product (if available in that state). Long term, DraftKings expects its DFS line which today is over half of its revenue to make up only ~10% of revenue, but is still important strategically to drive these said users into the ecosystem.

Growth Opportunities

The global gaming opportunity is massive, and most of it still occurs offline. The 2019 estimate for global gaming revenue is $456B. The largest segment is casinos, making up 35% of total revenue, followed by lotteries, machines, and sports betting.

Online and mobile contribute only ~12% of the total market, which implies that the industry is poised to be disrupted by more innovative business models. DraftKings innovativeness is front-and-center during COVID-19, and post-pandemic they are well-positioned to grow along with further online gambling legalization.

Esports. As we mentioned earlier, DraftKings Q1 revenue actually grew by 60% compared to last year. But due to sports being canceled, growth slowed to 30%. Even with sports gone, DraftKings has been able to quickly adapt their daily fantasy platform to new games. Most recently, DraftKings announced several games for eSports, such as League of Legends, Fantasy Madden, CS:GO, and Call of Duty.

We think eSports is compelling because it is natively online and fast-paced (e.g. League of Legend rounds are less than an hour), which is well suited for the DraftKings daily fantasy format. eSports highlights DraftKings’ ability to capture a nascent but quickly growing market opportunity, and we expect to see more growth in this area.

State-by-state online gambling legalization allows DraftKings to expand its proven business model (e.g optimized sales and marketing, cross-selling). The company originally estimated that 2020 revenue will be $540M, growing 25% compared to last year, which is driven by online sports betting legalized for incremental 10% of the U.S. population. However, this is before COVID-19, so we think our current estimate of $450M growing 5% is likely conservative.

The following year, revenue is expected to re-accelerate, driven by the continued growth of online sports betting and iGaming legalization. While there is some risk that legal actions take longer than expected to occur, we think, similar to eSports, DraftKings will be able to quickly capture the new opportunity once it becomes available.

Data science platform. While not as exciting as their consumer-facing brands, the infrastructure being built is equally compelling. DraftKings has collected over 8 years’ worth of data on over 4M players. This is incredibly valuable and still an untapped source of growth. Sports owners, leagues, and advertisers could use these data points to better services to their customers, increasing customer engagement and affinity (e.g. more loyal fans). This is a positive flywheel for the entire ecosystem.

However, we are still in the early innings of being able to use data effectively. Infrastructure must be built so the data can be used in a compliant and safe way. This is the data science platform that DraftKing has been building with SB Tech and its internal teams. Push notifications are one example of a recent success, where DraftKing has been leveraging earlier customer interactions to cross-promote new games and formats.

Competition/Risks

Direct Competitors: FanDuel (owned by Flutter Entertainment) is DraftKings’ major direct competitor in fantasy sports. However, there are many players vying for online gambling market share, like Penn National Gaming, which recently acquired media company Barstool Sports and has huge ambitions in the space. It’s not quite clear how this story will play out.

Increased marketing expenses due to limited cross-selling: Currently, 98% of DraftKings’ iGaming paid users have been cross-sold from other DraftKings’ product offerings. However, with slowed new user acquisition + engagement in the Daily Fantasy Sports and Online Sports Betting segments, DraftKings will have to spend quite a bit in marketing to build brand awareness to acquire new users directly to its iGaming business, instead of relying on the significant CAC advantage it initially had. Additionally as more states make online betting legal, more European incumbents (like Paddy Power, Bet365), will also enter, rising customer acquisition costs across the board.

Legal Risks: How quickly will online gambling become legal in individual states? DraftKings has experienced regulatory issues in the past, and state laws may thwart its ability to scale quickly. Future revenue projections assume 65% of the U.S. population lives in a state with legalized online sports betting (compared to just 24% today), and also assumes 30% of the population can legally participate in iGaming, compared to just 10% right now.

Key Questions to Ask Yourself (before we think you should buy...)

COVID has undoubtedly taken a hit on DraftKings’ core fantasy sports business, given the pause on all major sports. Do you think this revenue slowdown is risky, or do you think DraftKings will recover?

The online gambling space is growing quickly. Does DraftKings have an advantage in this space relative to their peers? Do you believe in DraftKings’ existing user base to continue converting into users of their online sports betting and iGaming products and give them an advantage in this space compared to their competitors?

Much of DraftKings revenue growth estimates are contingent upon state-by-state legalization of online gaming. How quickly will online gambling become legal in individual states? Do you think these regulatory risks pose an existential threat to DraftKings’ future revenue growth?

Our Take

We think DraftKings is an expensive stock but the market is going to expand very quickly as states change laws, and DraftKings is well positioned to benefit. We think DraftKings’ existing user base and their ability to execute so far has given them an advantage in this space and is a good bet long term. However, we think the slowed revenue growth is risky and will wait to see how much of an impact COVID has had on its revenue in Q2 and post-COVID before we buy.

Note this is not investment advice. Please consider doing your own research before making any investments!

If you’re finding this newsletter valuable, consider sharing it with friends, or subscribing and following us on Twitter if you aren’t already. If you have any feedback / comments / suggestions for what you’d like us to analyze, please share with us as well!