Stock Pick of the Week: Equifax ($EFX)

Stock Pick of the Week: Equifax ($EFX)

Remember the massive 2017 Equifax Data Breach?

For those joining in for the first time, welcome! Pocket Change is a newsletter where Tony + Karine keep track of and analyze stocks we think are noteworthy (and whether we should invest pocket change into). We’ve been friends since 2013, and have been sending each other stock suggestions and portfolio screenshots over the years. Pocket Change is our way of opening up the conversation and sharing these ideas more publicly. This newsletter goes out every weekend with our analysis and decision for a new stock.

Summary

✨Founded in 1899 by two brothers

💰Oldest Credit Reporting Bureau

📈Revenue: $958 million, +13% growth in Q1

👀147M people affected in the 2017 Data Breach

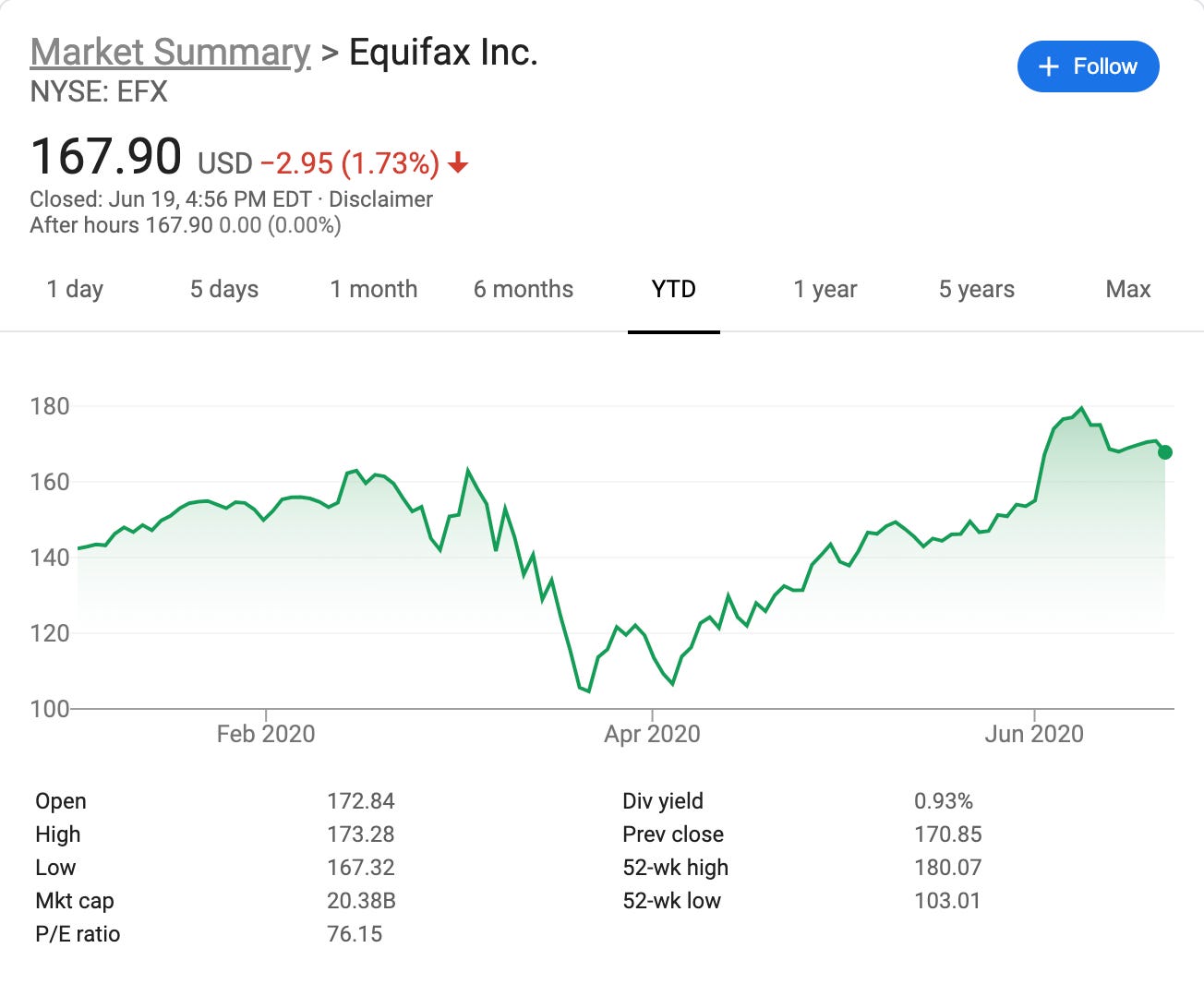

Remember in 2017 when Equifax got hacked and exposed the personal information of 147 million people? Perhaps you were even affected. Nevertheless, Equifax, one of the major consumer credit reporting bureaus, faced massive consequences when this breach was discovered and announced. The stock dropped 31%, wiping out $5.3B in market cap and revenue growth immediately stalled from +7-10% YoY rates the years prior down to 0-2% in the following two years in 2018 and 2019, as the company dealt with a heavy amount of negative public perception, lawsuits, and re-architected their platform to prevent further breaches.

For the first time in the beginning of 2020, we saw the first positive sign of recovery when Q1 revenue grew by 13% compared to last year. While this company is not as consumer-forward compared to the stocks we shared previously (Shopify and Nintendo), and you might still have lingering bad memories of the data breach, we think Equifax is a great business to own coming out of the COVID-19 crisis because Equifax plays an essential role in allowing consumers to access credit for homes and cars (as consumers flock from cities to the suburbs) and for businesses to process and assess new and returning employees (given the large swings in unemployment rates).

Why we Chose Equifax to Analyze

In addition to Equifax’s interesting position in the market amidst COVID and recent revenue growth, in terms of building our overall portfolio, we generally like to expose ourselves to a diverse set of industries with varying risk profiles. Because credit reporting has a long history in the modern economy and is essential in a credit-based society, we believe Equifax is an interesting pick to analyze that gives us more confidence in its stability compared to newer markets like ecommerce (like our previous pick Shopify), or more hit-based businesses (like Nintendo).

Some related news, if you had purchased just 1 share of each of the previously recommended stocks Shopify and Nintendo in the last two weeks, your portfolio would’ve grown $115 (+14%)!

Did you know?

Equifax started as Retail Credit Company in Atlanta in 1899 when Cator and Guy Woolford, two brothers from Woolford, Maryland, started to collect store credit payment habits, recording them as "Prompt," "Slow," or "Requires Cash,” and then resold the data as “The Merchant’s Guide” for $25. The business was extremely successful and was rebranded as Equifax in 1976 with the advent of mainframe computers.

Today, Equifax is one of the three largest credit reporting agencies, along with Experian and TransUnion. Equifax collects and aggregates information on over 800 million individual consumers and more than 88 million businesses worldwide, which ultimately generates an Equifax Credit Score that is used by potential lenders and creditors like banks, car dealerships, and credit card companies to assess whether an individual is reliable and can pay back loans.

Fundamentals

Enterprise Value (EV): $25 billion

Revenue (Q1): $958 million

Revenue Growth (Q1): 13%

EV/Forward Revenue: 6.6x

EV/Forward EBITDA: 20.4x

How they make money

Equifax makes money from a mix of subscription and transaction-based revenue. There are three main lines of business plus their international division.

U.S. Information Solutions (36% of revenue): The Equifax Credit Score and Report (as shown above) helps businesses such as banks and credit card companies extend credit to consumers and help them manage the entire process from loan origination, credit information to identity verification.

Workforce Solutions (27% of revenue): employment, income, and social security number verification as well as business back-office support (e.g. payroll, taxes)

Global Consumer Solutions (10% of revenue): credit information, credit history and identity protection for consumers

International (26% of revenue): Same as the first three lines of business but international in countries like Canada

At its core, Equifax is fundamentally a data business, which has more consistent higher returns and margins than an asset-heavy business because once you sell the data once, it costs minimal incremental cost to resell.

Growth opportunities

In the U.S. Information Solutions segment, Equifax generates credit reports for businesses to extend credit, which should be in high demand given that COVID-19 is causing migration from the city to suburbs. In addition, in the suburbs, people need cars to get around. Therefore, we will likely see more mortgage and car loan applications, which will positively impact Equifax. In fact, the credit report business was most damaged by the data breach but has since recovered and even grew 15% this quarter.

While Equifax is known for the credit report business, they also have a fast-growing Workforce Solutions segment which has The Work Number (TWN) flagship product. The TWN allows a third party (e.g. bank) to quickly verify a consumer’s income and employment information. The income and employment data solves a complex verification problem given the ambiguity caused by COVID-19. Even the government has trouble with this. In the May Bureau of Labor Statistics report, they stated that unemployment could be 23% higher due to misclassification error.

Because TWN has direct access to payroll information, it could provide an accurate picture of a consumer employment status in a potential unemployment claim form, mortgage application, etc. This business was not affected by the data breach has to grow to cover 1 out of 2 Americans with more room to grow.

Competitors / Risks

While Equifax is well-poised to grow, Experian and TransUnion are two other major credit reporting agencies that will benefit from the changes in the market. All three businesses collect consumer data from various institutions and sources, calculate a credit score and report based on their own proprietary models, and in fact, many banks and lenders use all three bureaus to assess consumer credit risk. Additionally, Experian and TransUnion have newer cloud-based platforms and have been more technology-forward in terms of adopting faster, better data processing capabilities. The biggest risk is that Equifax is the only credit reporting agency that has had such a major public breach, in a market that is built on consumer trust in its security and privacy.

Key Questions to Ask Yourself (before we think you should buy...)

Has Equifax put the data breach behind them? Can they protect their data from another breach or will public perception still remain largely negative?

Can Equifax return to growth in its core credit report business and increase their usage of The Work Number?

Can Equifax scale their product internationally and return the International segment to positive growth?

Our Take

Tony: I think the recovery story has teeth, and stock price should soon reflect the improving fundamentals and lower risk of data breaches. I think Equifax is a buy.

Karine: Given that Equifax has spent the last few years rebuilding its trust and infrastructure to prevent future data breaches, and looking at the recent quarter’s growth numbers, I think the stock is likely undervalued at the moment and that Equifax would be a smart buy.

* Note this is not investment advice. Please consider doing your own research before making any investments!

If you’re finding this newsletter valuable, consider sharing it with friends, or subscribing if you aren’t already.