Stock Pick of the Week: Pinterest ($PINS)

Stock Pick of the Week: Pinterest ($PINS)

Can Pinterest become a dominant advertising platform among the social media giants?

For those joining in for the first time, welcome! Pocket Change is a newsletter where Tony + Karine keep track of and analyze stocks we think are noteworthy (and whether we should invest pocket change into). We’ve been friends since 2013, and have been sending each other stock suggestions and portfolio screenshots over the years. Pocket Change is our way of opening up the conversation and sharing these ideas more publicly. This newsletter goes out every weekend with our analysis and decision for a new stock.

To receive this newsletter weekly, consider subscribing 👇

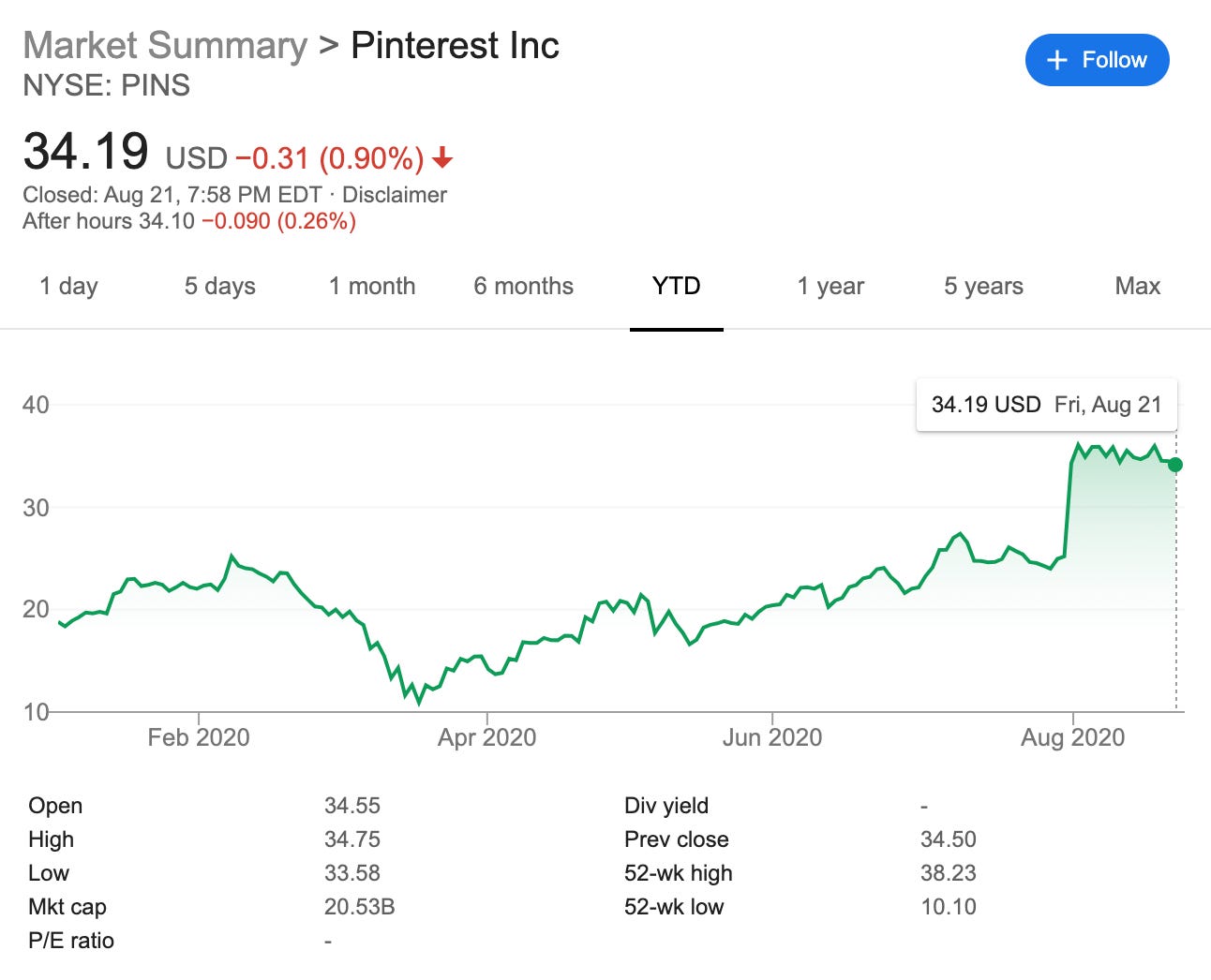

Summary

📍IPO’d at $19/share in April 2019

💰Enterprise Value: $19B

📈Q2 Monthly Active Users: 416 million, +39% YoY

👨💻👩💻Average Revenue Per User: $0.70

Instagram is to vanity as Pinterest is to inspiration. Both companies have a large role to play in the future of e-commerce. We covered Instagram, as part of Facebook, last week and highlighted their progress in shopping. Pinterest, however, is a much smaller company at only $21 billion market capitalization (vs Facebook at $760 billion), and earlier in their monetization efforts. Today they have 416 million monthly active users (MAU) and monetize at $0.70 per user. This is much lower compared to Facebook, which monetizes at $6.10 per user. While this means there is more risk investing in Pinterest, we think the future for Pinterest is promising and deserves consideration for your portfolio.

Did you know?

In May 2020, Pinterest launched a partnership with Shopify (another one of our favorite stocks) allowing merchants to upload their product catalog into shopping Pins (Pins are the basic unit in the Pinterest feed, similar to a Facebook post). On the last earnings call, CEO Ben Silbermann mentioned uploads grew 350% between Q1 and Q2, showing early signs of traction.

Fundamentals

Enterprise Value (EV): $19 billion

Q2 Revenue: $272 million, up 4%

EV/Next Twelve Month Revenue: 11.3x

Q2 Monthly Active Users: 416 million, +39% YoY

Average Revenue Per User: $0.70

COVID has hurt revenue growth in the short term, but the CEO said on the Q2 earnings call that in July, revenue growth had recovered to 50% compared to July 2019. He cautioned investors there is much uncertainty in the economy and they should be careful in extrapolating the 50% to the rest of the Q3.

How Pinterest makes money

Advertising. Similar to Facebook, Pinterest monetizes primarily through its Promoted Pins. Advertisers can promote both brand awareness and performance ads, with performance representing two-thirds of advertising revenue. Pinterest is continuing to invest in building out its advertising platform, as user growth acceleration has attracted more advertisers and ad dollars. Platform improvements such as the Today Tab and Shopping have enabled consumers to more seamlessly and consistently interact with brand’s products and ads. Ad platform improvements, like Shopping Ads, auto-bidding and dynamic targeting have also created a more robust Pinterest ad ecosystem with higher conversions.

Growth opportunities

International Growth. Pinterest has 321 million international MAUs, or 77% of the total base. However, it's growing faster at 49% compared to last year (vs 39% in the U.S.). The international app is currently available in predominantly English-speaking countries, so there are further opportunities to expand to the rest of the world. Snapchat, while slightly larger at $32 billion, is seeing only 17% growth in its user base. Pinterest expects to launch in South America in the second half of this year, supporting strong user growth going forward.

Monetization. Pinterest currently monetizes at $0.70 per user, far below Facebook, and so far has relied on large retailer and consumer packaged goods (CPG) for its advertising. However, there is less leverage in this model as each account requires a team of account managers, direct sales, etc to scale. We think that their ongoing efforts in self-serve infrastructure is promising. As CFO Todd Morgenfeld said in the last earnings call, they have accelerated their number of SMB advertisers benefitting from self-serve tools, contributing now to almost 50% of the revenue.

Pent-Up Demand. While the current economic environment has forced many retailers to pull back their advertising spend, we believe that the outlook is favorable for delayed spend in a few key categories, such as home decoration and furniture. Right now, given the record low interest rates, and combined with work-from-home due to COVID-19, have led a housing boom outside of large urban areas. The existing home sales are up 24.7% and homebuilder sentiment for new construction is at record levels. We think Pinterest will benefit from this short tailwind in new home ownership, as it leads to the opportunity to capture new users and resurrect existing users who might have churned.

Competitors / Risks

Other Social Media Giants. Pinterest faces much competition in the social media category, directly competing with Instagram/Facebook, Google, and Amazon. It may be difficult for Pinterest to become as big as its competitors in the short term. Additionally, some believe that because 70% of the app’s users are women and has a heavier focus on more “niche” categories like art supplies and hobbies, the company’s attractiveness to a wide range of advertisers may be limited.

Early in Monetization. Overall, Pinterest is still early in its monetization efforts. Revenue from domestic users declined by 11% this quarter from a year earlier due to a slowdown in advertising spend from the pandemic, and despite 72% YoY growth from its international users, Pinterest still derives $2.50 per user from domestic users, and only $0.14 from international users. Investments into the expansion, especially overseas, means that Pinterest will likely remain unprofitable for the foreseeable future.

Key Questions to Ask Yourself (before we think you should buy...)

Do you think Pinterest’s investments will allow it to accelerate monetization?

Is Pinterest an appealing platform for advertisers? Can it continue growing its ad revenue and compete with other platforms?

Our Take

We think Pinterest will like to crack the Facebook-Google advertising duopoly, and is well-positioned to establish itself a player in the growing e-commerce industry. Its focus on building out a more robust advertising ecosystem and sticker products like shopping make for a highly engaged user base. We would recommend buying the stock at the current valuation.

Note this is not investment advice. Please consider doing your own research before making any investments!

If you’re finding this newsletter valuable, consider sharing it with friends, or subscribing and following us on Twitter if you aren’t already. If you have any feedback / comments / suggestions for what you’d like us to analyze, please share with us as well!