Stock Pick of the Week: Snap ($SNAP)

Stock Pick of the Week: Snap ($SNAP)

At an all-time high...is Snap a buy?

Lots of new faces here...so welcome! For those of you that are new, let us introduce ourselves👋

Pocket Change is a newsletter where Tony + Karine keep track of and analyze stocks we think are noteworthy (and whether we should invest pocket change into). We’ve been friends since 2013, and have been sending each other stock suggestions and portfolio screenshots over the years. Pocket Change is our way of opening up the conversation and sharing these ideas more publicly. If you have any ideas, we’d love to hear them in the comments!

To receive this newsletter weekly, consider subscribing 👇

Summary

We had previously covered Facebook and Pinterest on Pocket Change. This week for our first post of the new year, we’re covering another favorite social media company - Snap.

Founded in 2011 by Evan Spiegel, CEO + Co-Founder, as part of a product design class project at Stanford, Snap has come a long way since then, albeit a bit rocky as a public stock. Debuting on the NYSE in March 2017, Snap first opened at $24, valued at a $33B market cap at the time. In 2018, Snap’s stock reached all-time lows below $7/share, and many wondered whether Snap could bounce back. Instagram’s clone of Snapchat stories took a dramatic hit on Snap’s stock. (Many at the time wondered if Evan was nostalgic for the $3B acquisition price Facebook had offered back in 2013).

But in the last year, Snap has really bounced back, closing at ~$53.57 last Friday at a market cap of ~$80B. Today, Snap is currently best positioned to tap into the “Snapchat generation”, as Gen-Z is still developing brand loyalty. Additionally, Snap’s vision as a next generation “camera company” has really begun to take shape, as evident in the launch of their “innovative and differentiated camera products” like Snap Minis, investments in AR/VR, and more.

Did you know?

In 2018, Snapchat tried to fix the bugs in its then Android app with no avail. At one point it became so bad that the Android platform was showing a sequential decline in daily active users (DAUs) from Q2 and Q3. The development team ended up rebuilding the entire app and launched it in mid-2019, re-implementing many of the successful features found in the iOS app. After the company resolved its “tech debt”, DAU growth rate-accelerated, particularly in the rest of the world. In India, a major Android market, the company saw 2x growth in early 2020. With better infrastructure in-place, the attention now turns towards adapting for regional cultural differences through customized lens and content.

Fundamentals (Q3 2020)

DAUs: 249 million in Q3 2020, compared to 210 million in Q3 2019 (18% YoY Growth)

Revenue increased 52% to $678.7 million in Q3 2020, compared to $446.2 million in Q3 2019 (+52% YoY)

ARPU was $2.73 in the third quarter of 2020, up from $2.12

User base penetration: 90% of 13-24 year-olds in US. 75% of 13-34 year olds in US.

How Snap makes money

Snap generates nearly all of its revenue from advertising, which includes Snap Ads and Sponsored Creative Tools like Sponsored Geofilters and Sponsored Lenses. A very immaterial amount of revenue is generated from sales of their hardware product Spectacles. In Q3 2020, $468M came from the US (70%), $107M (15% of revenue) from Europe, and $103M (15% of revenue) from the rest of the world.

Growth Opportunities

Improved Monetization - Many of the consumer internet companies are at the early stage of monetizing their user base, and could see further upside in the future. For comparison, in Q1 Snapchat and Facebook was at $2 and $10 per DAU respectively, implying a 5x upside. Snapchat has a large, engaging, growing audience and is investing heavily in building out their robust advertising platform and helping advertisers create content like Dynamic Ads, Sponsored AR Lenses and filters, that the Snap generation wants to engage with.

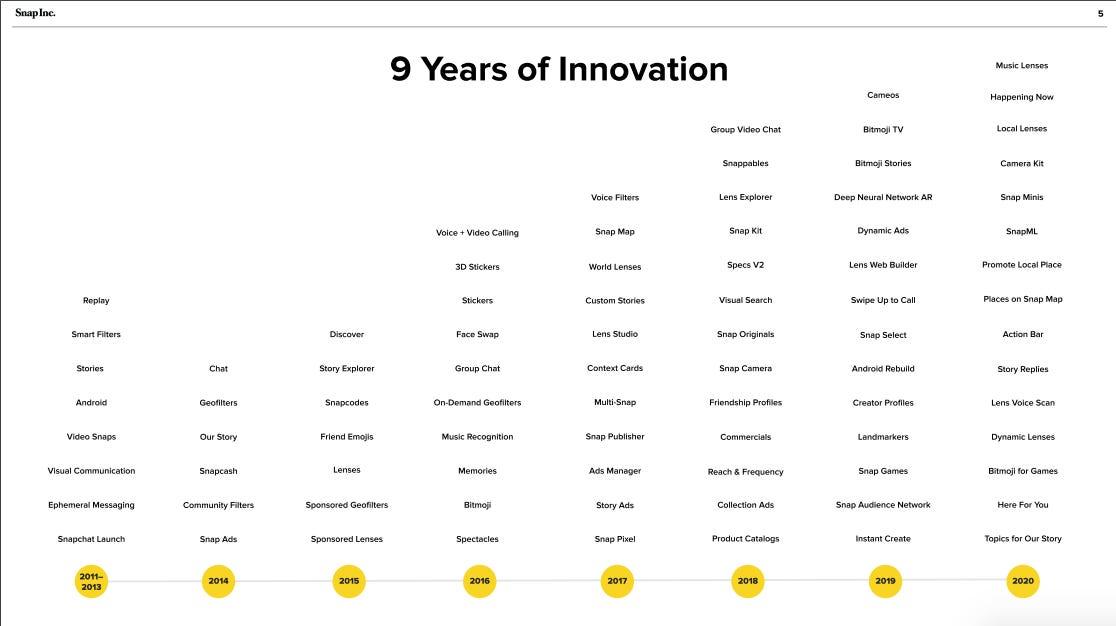

Investing in Innovation - A quick look at Snap’s innovation roadmap shows that Snap is heavily investing AR, premium content, gaming, maps, Minis, and content creators. Snap recently launched a $3.5M AR Creator Fund to help lure short-form video creators to create more AR content on the platform, hoping to emulate the success TikTok has had in helping creators build their careers on the respective platform as well.

Android + Expanding Geographies - According to Spiegel, there are over 2 billion Android devices worldwide. The company is early in the growth of its Android DAUs after rebuilding the technology platform. It is now focused on improving app performance, such as minimizing data consumption, and working with partners to localize the content. In the last quarter, Discover viewership increased 50% in India, and more users turned to Snapchat for premium content in Europe.

Competitors / Risks

Content Cost - Snapchat needs to invest in premium content to drive engagement and user growth. Its media partners provide some of the content in exchange for advertising revenue-share. The content cost is part of the cost of goods sold and it directly impacts the company gross margin. Quibi and its consequence shut-down shows us how risky the content business could be, although Snapchat as a distribution platform is more insulated from bad content. Furthermore, the company believes failed to combat inappropriate content could be a risk to its business. We have seen many companies in hot waters due to disinformation and content moderation.

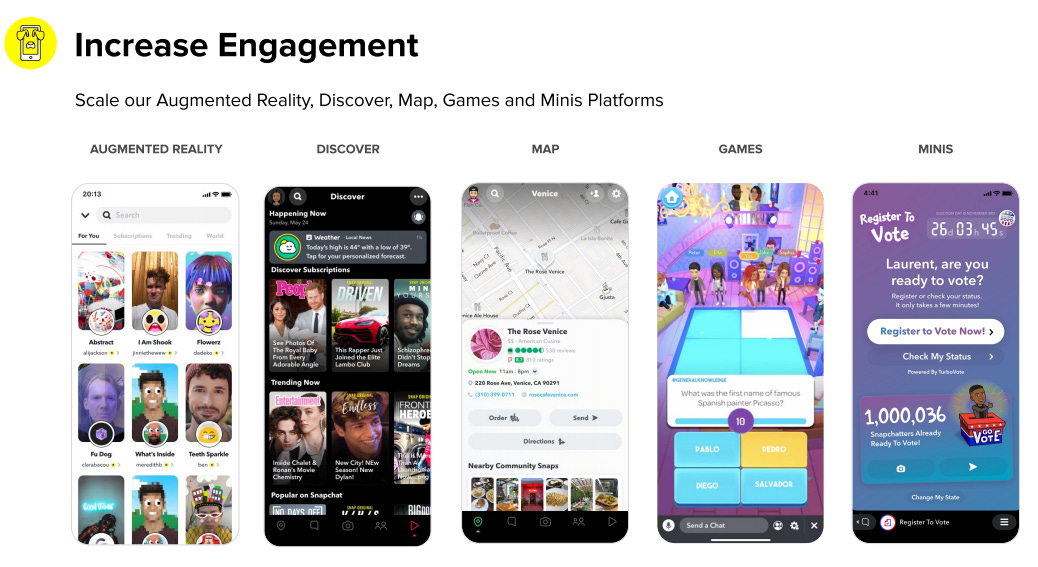

Other Consumer Internet Products - As Netflix famously stated in their investor letter, they compete with all types of consumer entertainment, across TV, web and mobile. Consumer attention span is short and there are many new apps being created each day, such as TikTok, Triller, Fortnite, etc and vie for attention. Snapchat needs to invest in developing new forms of engagement, such as expanding AR products, games and geo-focused features (e.g. Snap Maps) to remain relevant.

Valuation / Momentum - Snapchat is currently on a white-hot streak after blow-out results in Q3 2020. While it's impressive that Snapchat made a full “V-shaped” recovery in revenue, we caution investors on buying Snapchat at its current price, which is trading at 19x revenue for 2021 estimated sales growth of 40%. Any growth slow down could see shares tank, as we have seen with other high-flying names (e.g. Fastly).

Key Questions to Ask Yourself (before we think you should buy...)

Can Snapchat continue to build out new forms of engagement to stay relevant, such as Snap Maps and Snap Lens?

Can Snapchat continue to add premium content to attract user attention in new geographies while mitigating content risks such as disinformation?

Our Take

We think that Snap is currently on a white-hot streak compared to its social media peers and while well-positioned to continue growing its ARPU and innovation, we caution investors on buying Snapchat at its current price.

Note this is not investment advice. Please consider doing your own research before making any investments!

If you’re finding this newsletter valuable, consider sharing it with friends, or subscribing and following us on Twitter if you aren’t already. If you have any feedback / comments / suggestions for what you’d like us to analyze, please share with us as well!